Blog post

Joining up the dots

Energy Blog, 10 February 2023

What wind, nuclear and the cost of French electricity tell us about the wider economy for 2023?

Daniel Marshall reflects on how looking at the data of the French electricity mix between December 2022 and January 2023 tells us a lot about the impact of renewables and nuclear power, and how interconnected this is to the wider economy.

It’s human nature to look ahead and try to project a bit into the future. However, if we learned anything from 2022, then we should no longer be surprised at how unexpected events can come along and take us down a completely different path – although that’s probably true every year. Nonetheless, we still try.

In the French office, we spent some time discussing the year ahead, as we returned to work in January after the holiday season. In doing so, we also took a look at some historical data on the electricity generation mix in France over the end of 2022 and the first weeks of 2023. It’s only a short period of observation, but a very revealing snapshot all the same, with some significant implications for our wider macro environment in Europe.

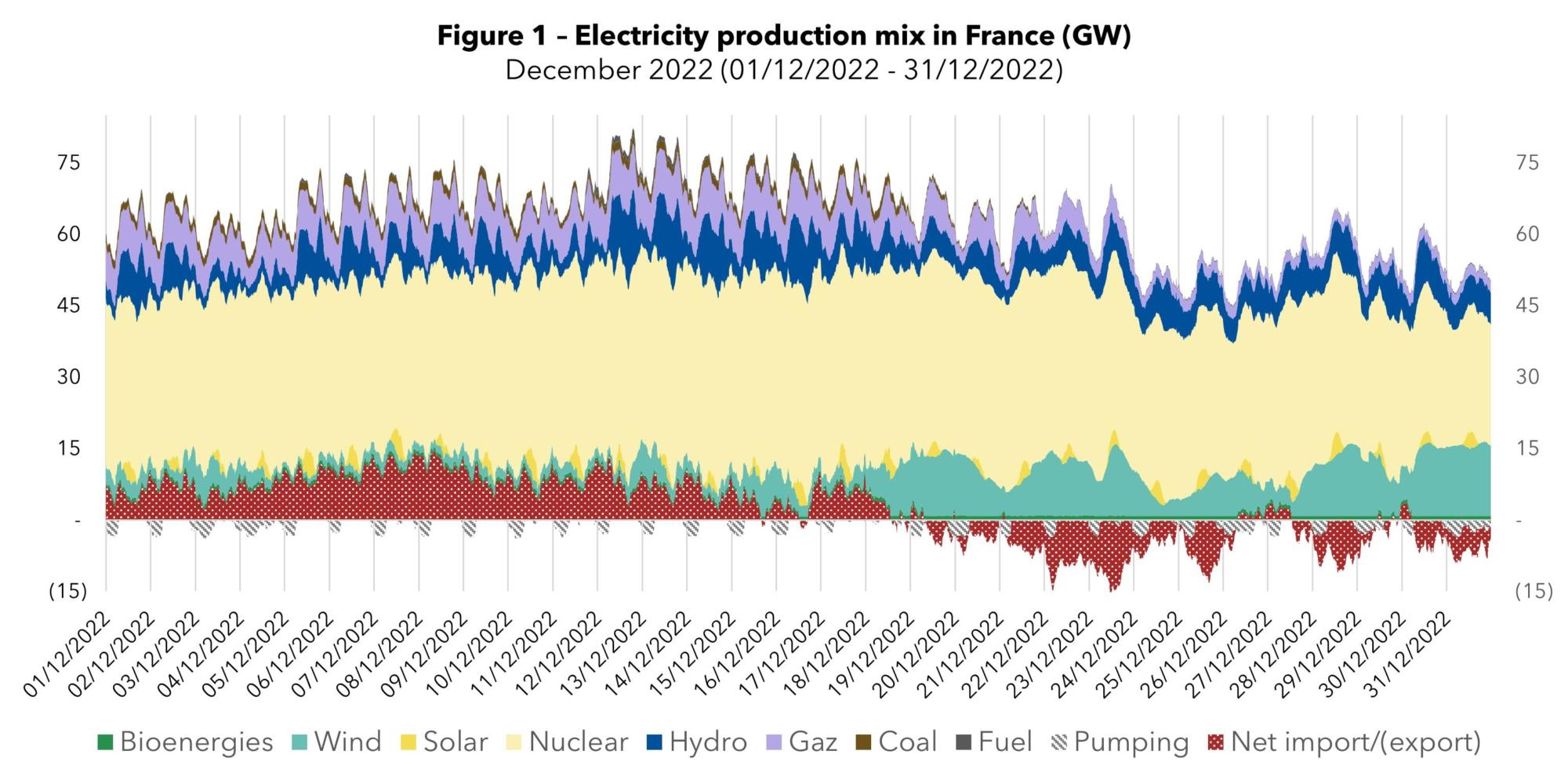

The figures below compare the electricity mix in France in December 2022 (Figure 1) and in January 2023 (Figure 2). The first thing you might notice is that you can see how a windy day means a huge contribution from wind to the French grid, despite offshore wind only recently starting to be a contributor here (with hopefully a lot more to come – we only need to look at the record contribution from wind to the UK grid recently, as an example).

Source: Data from RTE France, accessed on 9 February 20231

By end of December 2022, France recovered its position of net exporter of electricity, which is generally positive for Europe as a whole. We can observe here how that balance between being a net exporter or net importer of electricity is influenced by the day-to-day contribution of wind. This can have a major financial impact in France at moments when the nuclear fleet encounters issues, and in a situation where nuclear runs as normal and there is high level of wind, the opportunity is there to export clean electricity.

This situation of France as a net importer or exporter has a knock-on effect for French consumer electricity prices. EU measures on gas price caps are also going to be important, but for now they are not the determining factor in France for consumers. And this link to consumers is what leads us to start thinking about the impact on inflation, which at the start of the year was printing below expectations in France, and potentially driving sentiment on Eurozone inflation – time will tell if that is a correctly placed sentiment or not.

The FT commented2 last month that “lower energy prices helped push inflation down in France, as European stocks rose on growing expectations that inflation has peaked across the region. French inflation fell to 6.7 per cent in the year to December, against economists’ expectations of a slight rise following the 7.1 per cent figure recorded for November” […] Eurozone inflation is expected to drop into single digits for the first time in three months on the back of the fall in energy prices paid by the region’s households and businesses — a consequence of measures from the region’s governments to keep the cost of gas in check and warmer than usual weather in recent months.” The trend was further confirmed recently by the ECB as the FT stated3 “the headline rate [for the Eurozone] fell from 9.2 per cent in the year to December [2022] to 8.5 per cent last month”

This is “still more than four times the ECB’s 2 per cent goal” as the FT notes, but as a reminder, if inflation continues to taper then it will decrease the need for further ECB rate rises in 2023 and therefore rises in borrowing costs and relative returns, something which should be positive for greenfield renewables investment. Elisabeth Borne, the French Prime Minister confirmed this inflation outlook during a radio interview last month4, although at the same time she announced that the government will continue with its measures to cushion consumers (incidentally making a gas price gap far from neutral for the French government). It therefore does not require much of a stretch to link performance of the French electricity system to underlying borrowing costs and risk-free rates, which in turn have a significant impact on investor sentiment and returns in the same industry.

However, when it comes to inflation and the outlook in France and across Europe, we only wish it could be that simple. Multiple other factors will continue to be at play, but it’s worth highlighting two of the potentially more significant ones: global commodity stocks and China post COVID-19 reopening. Again, these two things are linked, so you might be starting to pick up on a theme here – the interconnectedness of seemingly unrelated factors in our operating environment.

Firstly, commenting on global gas stocks – It’s unseasonably warm, so we are using less gas than usual across the continent. That added to some very quick responses (including permitting and building of new LNG infrastructure – if only we could see permitting for renewables go so quickly…) has meant that stocks of gas across the EU have been rebuilt, which is in turn having a further dampening effect on electricity prices, and therefore inflation. For now, EU gas storage levels remain above their 80% target range, having been built back up to 90% at the end of 2022, and that’s good news, but we have seen how fragile that can be, and how expensive it can be to build back in the wrong market conditions.

Which brings us to the second important factor that may weigh heavily on EU inflation in 2023, and that’s the reopening of China. Lack of gas demand in China is one reason Europe has been able to rebuild stocks. In fact, dampened Chinese demand for a whole host of items has been one of the reasons we have not seen inflation take off further than it has. However, as the zero-COVID policy comes to an end, that is likely to change and the impact could be significant. That’s also against a backdrop where according to Goldman Sachs research5 we are sitting at the start of an “underinvested super cycle” for commodities, the most obvious sign of which is low inventory levels. Demand pressure on prices then seems like a significant risk to watch in 2023.

These two factors present clear upward pressure risks and increase volatility for inflation. Additionally, as European countries push towards further build out of renewables, neither is going to be conducive to helping stabilise pricing for capex or even visibility on supply chains.

It might be unusual that we talk so much about nuclear and commodities in a Green Giraffe blog. Nevertheless, the interconnectivity of our world means that our clients and us need to be close to this.

The snapshot of the French electricity mix from December 2022 to January 2023 shows how much the wind, the temperature and the state of the nuclear fleet can shift a huge country like France, from being a net importer to exporter of electricity literally overnight. Add in the effect of China reopening post COVID-19 and that of global commodity stocks, and the picture becomes even more complicated when considering the overall impact of these factors on the investment environment, including that crucial variable for many – inflation.

This instability makes the market less certain for investors. Anyone looking to finance or invest in projects will need to continue react to these heightened levels of volatility. Winners are likely to be those who can ride out the bumpy periods and be reactive and opportunistic when the right moments come along.

There is a lot more we could say for renewables in 2023, but a key takeaway from the data is the benefits renewables can bring and so we expect public and political support for renewables to continue to grow. As the world in 2023 will continue to be volatile and uncertain, we need to keep focused on delivering as much as possible on those energy transition goals – for decarbonisation, for energy security, and for our economic good.

Sources:

1 French electricity production data from RTE France, accessed on 9 February 2023 – available on www.rte-france.com

2 M. Arnold, A. Samson, “Falling French inflation sparks hope of end to Europe’s price surge”, Financial Times, 4 January 2023

3 V. Romei, “ECB set to raise rates despite fall in eurozone inflation”, Financial Times, 1 February 2023

4 Elisabeth Borne interviewed by S. Brakhlia and M. Fauvelle, Franceinfo, 3 January 2023 – available on www.francetvinfo.fr

5 Goldman Sachs Research, 2023 Commodity Outlook: An Underinvested Supercycle, 15 December 2022